- Blog

- |Managing Payroll

- >PAYE and Tax

- >HMRC RTI submissions

HMRC’s RTI Submissions Explained

Monthly payroll checklist

Confused about what the RTI system is and how it works? This guide covers everything you need to know about RTI submissions.

Let’s dig in.

What is an RTI submission?

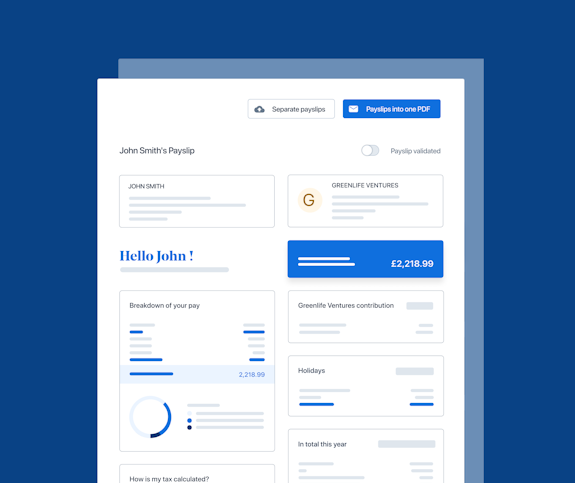

Real-Time Information (or RTI) is a reporting process under the Pay As You Earn (PAYE) payroll system, where employers report employee pay and other deductions to His Majesty’s Revenue & Customs (HMRC) each time they pay an employee.

Since its introduction in April 2013, RTI has helped employers save millions of pounds in administrative costs and reduce the time and effort required to report to HMRC.

In addition, since HMRC’s RTI submissions help employers record any changes to an employee’s personal details or employment status, they allow for a more accurate calculation of tax and National Insurance Contributions (NICs) due.

Employers typically use the internet or the Electronic Data Interchange (EDI) to submit their RTI to HMRC. However, employers who are exempt from the use of electronic communications can use a paper channel to file their RTI.

There are two types of RTI submissions you can make as an employer. These are the Full Payment Submission (FPS) and the Employer Payment Summary (EPS).

Let��’s break both of these down.

What is the Full Payment Submission (FPS)?

FPS is the main RTI submission employers make to HMRC whenever they pay their employees.

This submission should include the employee’s pay and any deductions from it. Employers need to make a full payment submission, no matter what an employee earns or how long they’ve been working.

A typical FPS should include your employee’s details, such as:

How much income tax and NICs should be deducted.

Their name, address, UK tax code, and National Insurance Number.

Information about their net salary.

Their employment status (whether they’re starters or leavers)

HMRC uses all the details provided to determine how much liability for each employee employers must pay at the end of the tax month or quarter.

You’re also expected to send in the FPS on or before the employee’s payment date. You can automate the task of sending your FPS to HMRC with payroll software.

That the FPS contains information about whether employees are starters or leavers is important because they often determine what other forms you might need to submit.

For Starters

After hiring a new employee but before paying their first paycheck, you should ask them to fill and answer the questions on the Starter Checklist. Doing so will help you ascertain the tax code that applies to that employee.

Sometimes, new employees will have their P45 form from their previous employer. If so, the information on the form can come in handy to know their tax code and determine how much tax they owe.

For Leavers

Whenever an employee is leaving your company, you should ensure you mark them as a leaver when sending the FPS to HMRC. You should also give them a P45 form to present at their next place of employment.

In the unfortunate case where an employee dies, you’re expected to submit the FPS with the employee’s date of death as their last day.

What is an Employer Payment Summary (EPS)?

An EPS is a part of RTI that's submitted to HMRC to inform them of any deductions to be made based on the calculations from the FPS.

An EPS is usually sent monthly. However, in some cases, you can send them every quarter or once a year, depending on the reason for the EPS.

Here are some of the most common reasons to send an EPS:

Construction Industry Scheme (CIS) deductions. This should be submitted once a month if you want to claim it.

Statutory Payments. This is for when you want to reclaim payments on statutory maternity, adoption, paternity, shared parental, or parental bereavement pay.

To inform HMRC if you don’t have any due payments for the month.

Like with the FPS, you can send an EPS through a payroll software.

RTI fines and penalties

As we already mentioned, you must submit the FPS on or before each employee’s payday and EPS as the need arises.

Failure to submit the FPS on time will attract a penalty from HMRC. HMRC will fine you depending on the number of employees you have.

Here’s what the fine/penalty for different company sizes looks like:

Companies with 1-9 employees will have to pay £100

Companies with 10-49 employees will have to pay £200

Companies with 50-249 employees will have to pay £300

Companies with more the 250 employees will have to pay £400

HMRC can add more penalties if you still fail to file your RTI after three months.

Aside from turning in your FPS late, you can also be fined for inaccurate in-year RTI submissions and late PAYE payments.

How does PayFit help businesses with RTI submissions?

Payfit is an HRMC-recognised payroll platform that automatically handles all RTI submissions (FPS and EPS) on your behalf. So now, you’ll never have to worry about keeping your employee records intact (to avoid duplications and inaccurate tax calculations) or sending the FPS and EPS on time.

Book a free demo today to find out how Payfit can help you.

A UK 4-Day Working Week - Thoughts On Labour’s Plan

Running payroll - A Guide For New Businesses

The Alabaster Ruling & Maternity Pay - A Guide For Employers

The End Of Zero Hours Contracts? Implications For Businesses

What is the HM Revenue and Customs Starter Checklist