- Blog

- |People management

- >Salaries & Benefits

- >salary advance

Salary Advance Schemes : The Pros & Cons For Your Business

Salary calculator

The ‘war for talent’ continues across the UK recruitment space. HR and strategy teams are having to get increasingly creative with the compensation, benefits and perks offered in order to attract and retain the best talent.

One such perk available to employers is the salary advance scheme - in other words, allowing employees to access part or all of their salary before the standard company payday.

Despite the benefits for both employees and employers, there are aspects about providing any advance on salary that you’ll need to consider. There are also common misconceptions around how salary advance schemes work, which we can hopefully clear up for you in this article!

What do we mean by ‘salary advance’?

As the Cost-of-Living crisis continues to bite, employers are looking at new ways to help support their employees’ financial wellbeing. One option that is becoming increasingly popular is that of salary advance. It’s something that Tesco launched at the end of 2022 ‘to help (employees) with unexpected or large expenses’.

The concept of a ‘salary advance’ refers to a short-term loan provided ahead of payday to an employee, sometimes via a specialist lender but usually not, with an agreement that any money borrowed will be paid back through the employee’s next paycheck. Signing up with a salary advance scheme provider is one option, however there are other options available (as we’ll come onto below).

How does a salary advance scheme typically work?

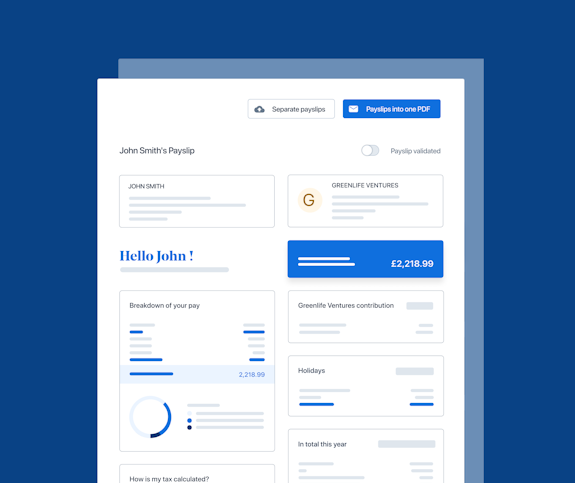

If the way that a UK salary advance scheme works sounds easy, that’s because it broadly is. Having said this, there are some important steps for employers to take in order to get a scheme set up. In other words, it isn’t recommended to just pay your employees ad hoc pre-payday amounts, and adjust their next payroll accordingly. This can overcomplicate things from a payroll perspective, takes time, and is an error-prone approach. However, certain payroll software providers can account for advances on salary and adjust everything automatically on the next payroll.

The first step in initiating any advance on salary using the external provider method is to sign up with a suitable partner. You should give your employees access to their own login for the tool in question, which will show how much is available to take early, the amount being calculated from work already done in that particular pay period. Most only allow staff to take up to a maximum of 50% of their salary for that period, as well as restrict how many times the scheme can be used.

Once the amount is chosen, fee deducted (usually £1-2) and money deposited in the employee’s bank account, you will pay back the salary advance company the loan amount and adjust the employee’s next payroll amount accordingly.

But this is quite a manual, complicated way of running a salary advance scheme.

Some payroll software providers, PayFit included, help facilitate advance payments to staff that will automatically reflect in the upcoming payslip, with all tax and deductions also calculated (automatically) as well. The advance payments will most likely have to be made via bank transfer yourself, but at least you can be sure that you remain compliant with your reporting commitments to HMRC.

What are the benefits of a salary advance scheme?

The benefits of a salary advance scheme can be felt on both sides of the fence. A concept in its infancy, at least from an official perspective, it can provide a competitive advantage to employers, as well as financial support and peace of mind to employees.

For employers

Improving the wellbeing and quality of life for employees is a key metric by which HR teams are measured. To this end, offering a salary advance scheme can help tick that box. Not only is it a great way to support and retain existing employees, but can be a great method for attracting new staff at the recruitment stage. Not many companies do this currently, so those that are prepared to do so can gain the edge over competitors in the war for talent.

Improving your employees’ financial resilience through an advance on their salary can help improve productivity and engagement as well, as staff will be less distracted, more engaged, and calmer in the workplace.

For employees

It’s no secret that the Cost-of-Living crisis is hitting people in the pocket, but it’s impacting upon their mental and physical health too. By offering a salary advance scheme, employers can help alleviate this, and support staff in taking control of their finances a little better. Financial control and improved mental health go hand in hand - and even if staff never use the scheme, being aware of the availability of that safety net can help to improve their mental wellbeing all the same.

And what are the drawbacks?

Doing anything to complicate the often complex payroll process can put a strain on your resources and runs the risk of tax errors being made. This is particularly true if going down the salary advance provider route, however this is negated when managing a scheme via payroll software such as PayFit.

Making unplanned payments to staff, whilst they even out in the next payroll, can impact upon cash flow, especially in small businesses where things are constantly tight.

If working with a salary advance provider and sharing sensitive employee financial information, you run a heightened risk of a data breach, which could permanently impact upon your company’s reputation and mean you incur penalties.

And if looking at it from the employee perspective, becoming reliant on salary advances could actually end up negatively impacting their financial and mental wellbeing, as their pay packets will be lower than usual and this could mean bill, rent or mortgage payments all going out around the same time are impacted.

What employers need to consider when offering advances on salary

Whilst a salary advance scheme is relatively easy to implement, particularly when going down the route of administering it via payroll software and manual bank transfer, there are some things to consider.

UK salary advances are not an FCA-regulated lending product, seeing as they aren’t classed as credit. For the same reason, employer salary advance schemes are also not governed by the Consumer Credit Act 1974.

And if you decide to partner with a salary advance provider, they are required by law to adhere to the Data Protection Act 2018, so you should make yourself aware of the principles by which they will manage sensitive employee data.

Deciding if a salary advance scheme is right for your business

In short, if your business is financially stable with good cash reserves, reliable cash flow and robust processes in place - for example around the management of payroll - then there is little reason to stop you from implementing a scheme.

PayFit can help make recording advance payments to employees a breeze, as well as ensure that future payslips are accurate, and that the correct information is reported to HMRC for tax purposes.

Find out what else it can do for your payroll capabilities by booking in a demo with one of our product specialists.

A UK 4-Day Working Week - Thoughts On Labour’s Plan

Running payroll - A Guide For New Businesses

The Alabaster Ruling & Maternity Pay - A Guide For Employers

The End Of Zero Hours Contracts? Implications For Businesses

What is the HM Revenue and Customs Starter Checklist