- Blog

- |People management

- >Pensions

- >Pension contributions

Three Factors That Impact Pension Contributions (And How PayFit Helps)

Workplace pensions guide

National Payroll Week has started, and of course, we are celebrating all the payroll professionals out there! In the payroll world, pension schemes are a key element.

We have previously written about five things everyone should know about their pension. This article explains factors that may impact an employee’s pension contributions and how PayFit can help organisations set up and manage pension schemes.

Who has to contribute to a pension scheme?

Anyone between the age of 22 and the state pension age, earning a minimum of £10,000 per year, and working in the UK must be enrolled in a pension scheme with a minimum contribution of 8%, 3% of which must be contributed by the employer.

The number of employees enrolled in a pension scheme used to be less than 2.5 million when auto-enrolment started; however, in 2021, over 20 million people are now enrolled in a pension scheme.

When we covered the facts about the pension scheme in our previous article, we briefly touched on salary sacrifice. Here, we go into more detail about salary sacrifice and how it can impact pension scheme contributions.

What is salary sacrifice, and is it suitable for all?

A popular way of contributing to a pension scheme is through salary sacrifice, which means that the employee gives up part of their gross salary, and the employer pays this straight into their pension. In most cases (and the main reason salary sacrifice is so popular), both the employee and employer will pay less tax and National Insurance.

Salary sacrifice may not be appropriate for all employees, though. As salary sacrifice deductions reduce gross pay, this also reduces the pay for National Minimum Wage (NMW) purposes, so employers need to be mindful when operating a salary sacrifice scheme that employees are not taken below NMW. If this does happen, an employer might agree to pay more than the minimum amount required to cover some or all of the employee’s pension contribution, or the employee may be offered an alternative way of contributing to the scheme.

It’s important to note that statutory payments and furlough pay cannot be sacrificed, meaning employers will likely need to cover the sacrificed amount during these periods. Salary sacrifice arrangement also means changing the terms of an employment contract and can also impact entitlements to statutory payments.

How do statutory leaves impact pension contributions?

So, we now know how salary sacrifice impacts pension contributions, but what about when employees take statutory leave? During paid statutory leave such as statutory maternity, statutory paternity or statutory adoption leave, the employer and the employee need to carry on making pension contributions.

The employee’s contributions will be based on statutory pay received and may be less than they would normally contribute. Still, the employer pays contributions based on the employee’s salary as if they were not on leave.

Does being on furlough impact pension contributions?

Now, after looking into traditional statutory leave, we can’t leave out the impact of the new “F-word” that has been on everyone’s lips these past 18 months, Furlough!

Furlough has been one of the most significant changes in UK payroll legislation for many years. This time last year, we saw over 2.5 million employees within the workplace pension age bracket receiving a proportion of their wage through the Coronavirus Job Retention Scheme. Three months earlier, the figure was over three times higher at a staggering 8 million employees. But what impact did being on furlough have on pension contributions? Pension contributions were based on furlough salary, or what was previously contractually agreed, which means employees on furlough may have paid less into their pension and that the employers may have contributed less.

It’s important to note that employers still had to pay at the agreed rate, i.e. 3% if 3% was contractually agreed, based on the same earnings threshold.

How does PayFit help businesses with pension scheme management?

There are many things that employers need to take into account when it comes to a pension scheme, such as whether it will accept their staff, how much it will cost, whether it uses the best tax relief method and whether it will work with their payroll process. To keep things a little easier, here is how PayFit can help.

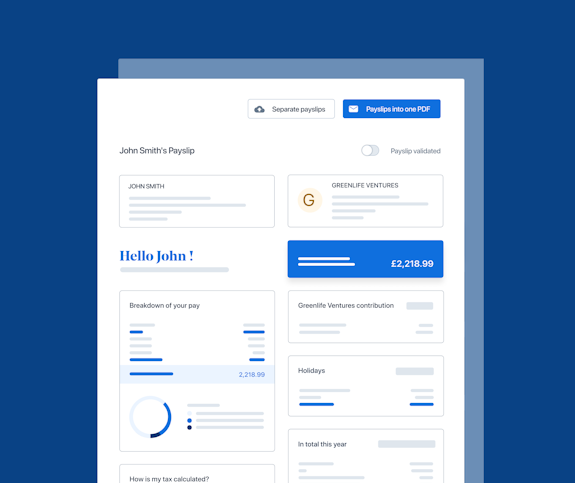

PayFit handles a wide range of pension providers

With PayFit, you can manage new joiners, leavers and monthly pension contributions all from one central place. Our software generates pension files for a wide range of providers, and we even offer full integration with certain providers. In this case, all you need to do is enter the employees’ information, and PayFit takes care of the rest - new joiners are automatically enrolled, and files are sent directly to the provider.

Pension providers PayFit integrates with

AVIVA Workplace Pension

NEST

NOW: Pension

People’s Partnership, previously The People’s Pension (B&CE)

Smart pension

Providers PayFit generates a file for

AEGON (Arc, Retireready, Smarterpay, Smartpay)

Ascot Lloyd Benefit Solutions

BCF Trust

Collegia

Cushon

Hargreaves and Lansdown

Legal and General

Penfold

Royal London

Scottish Widows and Scottish Widows AssistMe

Standard Life

The Creative Pension Trust

TPT Retirement Solutions

True Potential Investments

Auto-enrolment is automated in PayFit

PayFit also carries out automatic enrolment assessments based on employment status, age and earnings to determine whether or not they’re an eligible, non-eligible or entitled worker.

If an employee is eligible, you’ll be asked to add that employee to a pension scheme with at least a 3% employer and a 5% employee contribution (alternatively, you can postpone this up to a maximum of three months).

Where an employee isn’t eligible for a particular month, our software will continue to assess their status on a monthly basis so we’re ready to send out any mandatory messages if they do become eligible.

Salary sacrifice is easily managed in PayFit

While salary sacrifice is a tax-efficient and cost-effective way of deducting both employee and employer pension contributions, some employers find it daunting and prone to errors. With PayFit, setting up a salary sacrifice scheme is easy, and calculations are automatic, considering all variables impacted.

Interested in finding out more? Why not book a call with one of our product specialists?

PayFit disclaimer

The information contained in this document is purely informative. It is not a substitute for legal advice from a legal professional.

PayFit does not guarantee the accuracy or completeness of this information and, therefore, cannot be held liable for any damages arising from your reading or use of this information. Remember to check the date of the last update.

A UK 4-Day Working Week - Thoughts On Labour’s Plan

Running payroll - A Guide For New Businesses

The Alabaster Ruling & Maternity Pay - A Guide For Employers

The End Of Zero Hours Contracts? Implications For Businesses

What is the HM Revenue and Customs Starter Checklist